Our account of the Subprime Crisis dates back to August 2007. But the incident called on our attention only following the streams of news on the write-downs in the billions by the major banks on losses as a result of the crisis which was already some months later. We chose to play by the ears.

Besides, the markets made only mild retreat as you can see from the chart above. It refused to succumb to the intoxication of the banking sectors. It was not until the coming to light of Lehman’s collapse and AIG, Fannie Mae and Freddie Mac’s desperate SOS calls for US government bailout that we only began to see that something was indeed very wrong. It became obvious that it wasn’t just a common flu, but we were quite lost at what to expect and honestly, we never heard of anything like this before. We were not ready to take any action as yet, not until we noticed the sell down on blue chips, which was sometime in late 2008. That finally raised our whiskers. We were sure, by experience from empirical observations that almost certainly, whenever there was a wide-base sell down on a big basket of blue chips, the market was apt for an across-the-board ‘devaluation’. We were especially convinced of an impending meltdown when the sell down finally took place because we were questioning the ‘strange’ resilience of stock prices under such dire catastrophe at the early onset. It was a ‘confirmation’ that the tidal waves had reached our shore. We quickly worked out the downside potential on a handful of selected stocks using a method called ‘reverse-calculation’ (which we will show on the chapter of pricing and valuation) with a few scenarios so that we could act in time to protect our portfolios. This method enabled us to objectively churn out a set of precise figures that would otherwise be too conservative had we depended on our gut feel. It helped us measure and see in a more precise way the absolute downside based on our scope of assumptions. We liquidated our portfolios, saving some 40%-50% on potential losses.

Following 29th September 2008, the faithful day when Wall Street recorded its largest intraday of 777.68 points, the Dow continued to plunge further with another 2434 points by 22nd October 2008 as the Democrats and Republicans poured cold and hot waters over the markets with their indecisive resolution of the massive US$700 billion package to save the economy.

continuing...

In the illustration to follow, you will see that we took the exact same steps we have taught you in this chapter. Let’s see how we attempted to predict the stock market bottom, first by checking on the economic situation and then followed by analysing the past and present episodes so that we can reasonably conjecture the highest possible course of outcome of a new episode, uncensored:

On 31st Nov 2008, we decided to chronicle the above to perform a systematic analysis on when and where the market would bottom out. We subsequently wrote an article with the above chart attached and disseminated to various media and our fellow mates. Now, we explain our thought process and how the final conclusion was arrived at.

Step 1 of 4: Preparing the stage for the analysis.

The initial stage of analysis involved a simple preparation of making a chronicle on the past and the most current so that we could make a ‘prediction’ on the future. The past and present theme and their corresponding episodes were not so much of a problem as it only required some searching on the internet for relevant information. Next, we denoted them with a plus or minus sign on the chart accordingly. A plus sign represents the overall state of prevalent positive factors at work during the episode and a minus sign represents the negative. The two signs( plus and minus) are placed side by side whereby a bigger plus aside a smaller minus means that during the episode, there are more positive factors dominating the market place than negative and vice versa.

Step2 of 4: Checking if the track of economy is intact.

Our analysis began with on the economy. The Subprime Crisis (SC) had put everything out of place. The answer was obviously no; all major pillars damaged. There was a huge ‘minus sign’ prevailing and daunting the market place. This step was straightforward and quick given the obvious. We couldn’t be too wrong about the state of economy with all the talking heads reiterating that it was an unprecedented event of history each and every day.

Step3 of 4: Figuring out when the dust would settle.

So the next important question to ask is, if you still remember: how long does it take for the dust to settle? How long will the episode last? In order to figure that out, you need to look at the plus and minus signs again. We answered the question by considering the following possibilities:

1. The big ‘minus’ may be gradually neutralised by the sum of effects from many small ‘pluses’ over a long period of time;

1. The big ‘minus’ may be quickly neutralised by the sum of effects from many small ‘pluses’ over a short period of time;

2. The big ‘minus’ may be gradually neutralised by the sum of effects from a few big ‘pluses’ over a long period of time;

3. The big ‘minus’ may be quickly neutralised by the sum of effects from a few big ‘pluses’ over a short period of time.

Logically, to get the economy back on proper course, there must be enough or near sufficient positivities to turn it around. In our terms, we call it the ‘neutralisers’. In the case of SC, they came promptly as stimulus packages from respective countries to prevent the collapse of the global banking system. And so the whole episode entered into a ‘neutralising phase’ where the corrective measures were infused to stabilize the wobbly economic conditions. And it is a subtle and subjective interpretation of whether the ‘medicines’ would work. We believed it would for a few reasons:

1. Unlike the 1920’s Great Depression where it was left to heal its wound, the respective governments take a proactive stance on preventive measures. And besides, with decades of accumulated financial knowledge and experience, the new governments have more than adequate tools and know-how on reviving an ailing economy.

2. The infusion of the stimulus packages is of real hard money, and that meant the fresh money is going to trickle into the economy, part of it filling up the crater of losses and part goes to creating jobs through national investments;

3. The stimulus packages comprise of money that will get the banking system to continue its functions in the credit market that keep households and businesses afloat to ease the credit tension, keeping jobs.

4. The promptness of coming to the rescue by respective governments offer some form of assurance that in turn prevent the consumers’ confidence to deteriorate further and that’s by far, in our opinion, the most important pillar of the economy.

As you can see from the chart, the four shaded areas represent the episodes. The second half portion of the chart was labelled with our ‘predicted’ episodes of themes into the future from the point marked by ‘YOU ARE HERE.’ From this point forth, it involved the skill set of projecting the episodes and the corresponding themes.

On the back of the above rationales, we were convinced that the ‘dust’ would settle very soon because the pluses and minuses cancel out each other. Recall that we referred to the ‘dust to settle’ as concerns to ease. So do not confuse ‘issues of concern’ with the actual outcome of the economy. We are not making any form of claims that we could work out the complexity of how the stimulus packages or course of preventive actions taken by respective governments would eventually turn out. To make sure that you are still with us, we need to clarify that our study was principally on the psychological aspects; the easing of concerns or fear amongst the investing public. Therefore, you may note on the chart, the two equally big plus and minus sign which represents the neutralising of prevailing issues of market concerns. You should also note that we were careful in conjecturing the neutralising actions by extending the time period to allow room for the remnant impact from the SC which we believed would continue to fill the headlines simply by taking a count on the companies that had already made their quarterly earnings reports and anticipating more bad news to come from those companies which were waiting in reporting queues, factoring them into the projection. (There are a lot of websites that provide a list of companies pending results release.) On that basis, we expected that the good news of governments’ rescue plans would be weighed down by the coming bad earnings reports. And so as illustrated on the chart, we deduced that the market would take a choppy sideway movements as the good and bad news crashed. We were also able to make a forecast on the length of time because we could easily find out just how many more companies had yet made their bad news public and the last one to do so would be the last big bad surprise, as far as the period of our analysis is concerned, and hence, the dust should start to settle from then forth as the worst gradually tapers off. Logically, if we were right about when the worst news would hit the market, we could safely expect the stock market to rebound from the level which, in our opinion, had over

Step 4 of 4: Looking for the ‘Sweet-Spot’.

On our final conclusion which is the whole purpose of making the analysis; attempting to catch the market bottom, we now refer to the box of ‘future episode’ on the chart where we forecasted a ‘faster-than-expected’ stock market rebound with a clear and steep upward arrow drawn. All these were done and original excerpt and chart are presented without tampering of any material. Therefore, the lesson here is that if you learn to take the pulse of the economy, know what are episodes of the stock market, learn the concept of the ‘settling of dust’, apply these steps and you should be able to find the ‘sweet spot’. It’s really simple, but we still need to highlight that all events are unique and the way by which everyone interprets often vastly differs and hence the deduction varies consequently.

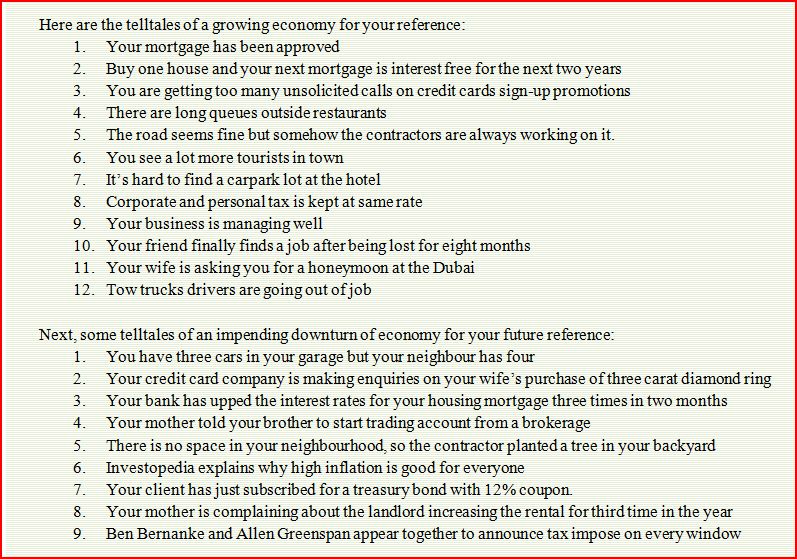

We have made a list of popular theme and the telltales of the economic situations as follows:

More about themes: Once you have identified the main theme, you need to use all your brain juice to figure out two things; you should first address the more important concern of whether the big trend is still intact by examining the potential effect or impact on the economy, not the stock market as yet. You do that part of analysis later (discussed on the next chapter on Grand Clock Theory™). Next, you need to figure out just how long will the episode last. You will see how to do that as you read on.

Remember you only need to figure out the magnitude or severity of the ‘issue’ by asking one simple question: As a result of the event, will the state of economy be altered? If the answer is a straight no, the economy remains steadfast, then standby your buying limits. But if the answer is yes, then you’d first need to assess the potential damage and the period for the dust to settle down; the ending of the episode. Note ‘dust-to settle’, not literal recovery. Dust- to-settle means the concern or tension to ease. The ‘Sweet Spot’ for buying is in the period between the ‘settling-of-dust’ and just before there is any clear sign of recovery; it is the period between the ending of current episode and the beginning of a new episode; the window period of the closing of the chapter of the current theme and opening of a new chapter of fresh market theme. Once you sense that moment, standby to execute your trade ideas. (Note that however you may not have sufficient information to form an immediate opinion or conclusion at times. If that is the case, you will need to keep a close look out and update as much and as quickly as possible.) Remember that you keep checking the status of economy for direction, not the stock market. One important note is that the stock market often gives you a very different story in the way it reflects price elements. It takes a much seasoned trader to read the market movements that involves too much of psychological game. That’s why we need you to emphasise on reading the economy and not the stock market. Being a wise player of the market, you should take advantage of market opportunity when event and price are in disproportion (read pricing and valuation on how you calculate and factor news into prices) As long as the economy track remains intact, barring unforeseen hiccups, the market will quickly find its way back. There is no chance to think twice about an obvious discount; the market rule is that anyone who comes to the market looking for the obvious pays the premium.

Now, let us test the model on another by simulating a bad ‘episode’ through our imagination. Perhaps, an eight on Richter scale somewhere in the northern hemisphere and the news quickly makes its way through the internet onto the screen of every single traders or investors. To recall, we check that the economy remains intact. It is likely to be fine unless the quake significantly disrupt or destroy important businesses that are deemed as pillars of the given economic structure such as an entire fleet of car manufacturing factories or banking district. In this case, it is still a temporary shock to the market, in our opinion. We can be quite sure that the market will tumble on such news, but let’s stay calm for a moment and think:

1. Yes, the damage is real;

2. Yes, the operations are disrupted and will not be functional until the facilities are rebuilt;

3. Yes, people died in the unfortunate event;

4. Yes, the CEO of a listed company was also unfortunately killed;

5. Yes, it is really a bad news.

Now, time for the ‘buts’:

1. But the rest of the economic functions are still intact;

2. But the world will not reduce spending; consumers’ confidence is still intact;

3. But the monetary losses of the companies affected by the quake are limited to the fixed assets that can be rebuilt and some temporary loss of business as a result. Customers will not abandon them as a result. The business model is well intact;

4. But the other stocks that are totally unrelated to the quake have also fallen as a result of the outbreak of news;

In above hypothetical scenario, note that all fundamentals remain largely intact. In fact, the lesson from this ‘mock-up’ is that as long as the main pillars of economy remain intact, the market is surely in for a mere knee-jerk reaction which means its great opportunity for the savvy. Remember also the ‘sweet spot’; ending of current episode and beginning of new episode. We end the chapter with the summarised steps:

0 comments:

Post a Comment